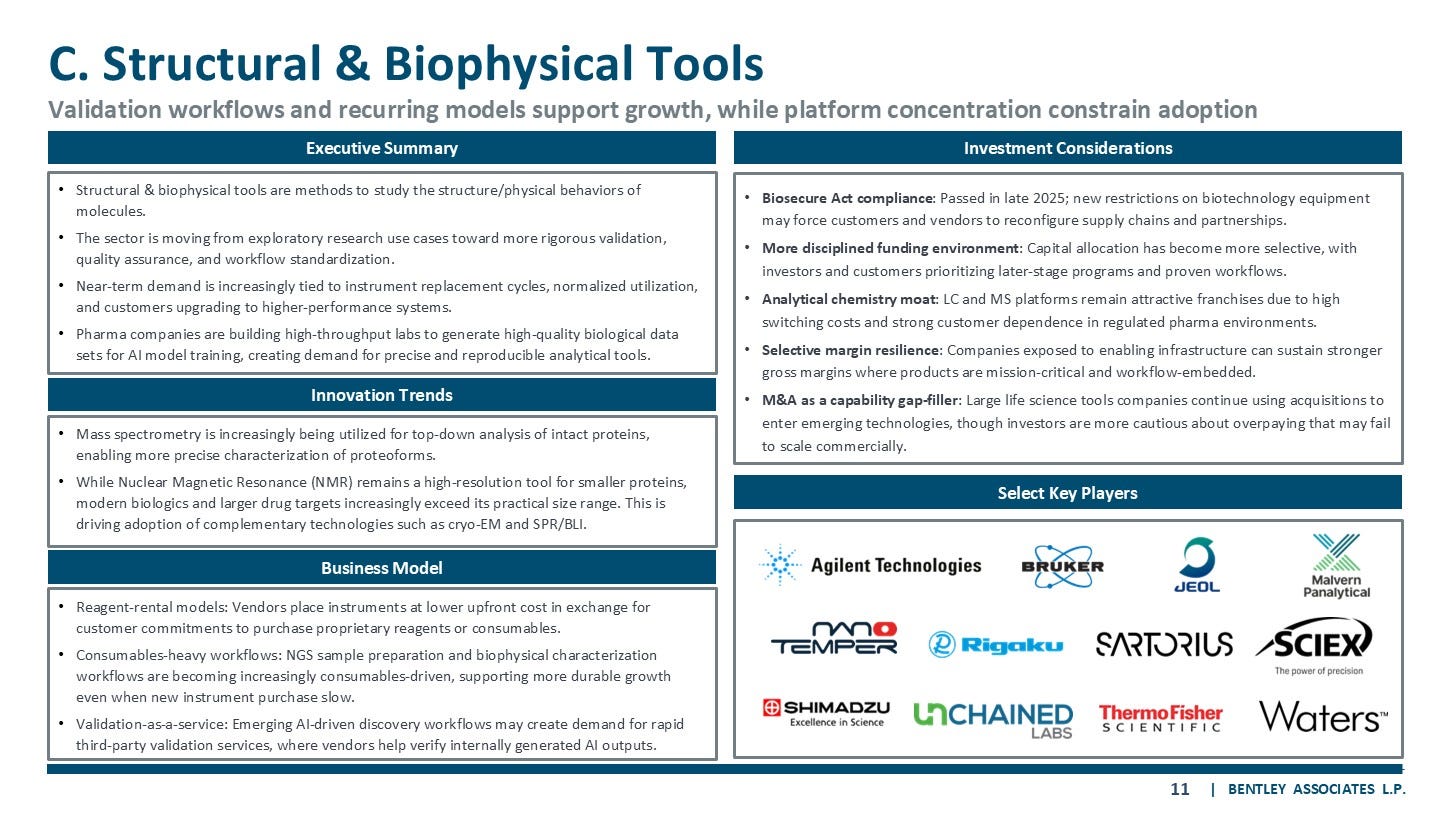

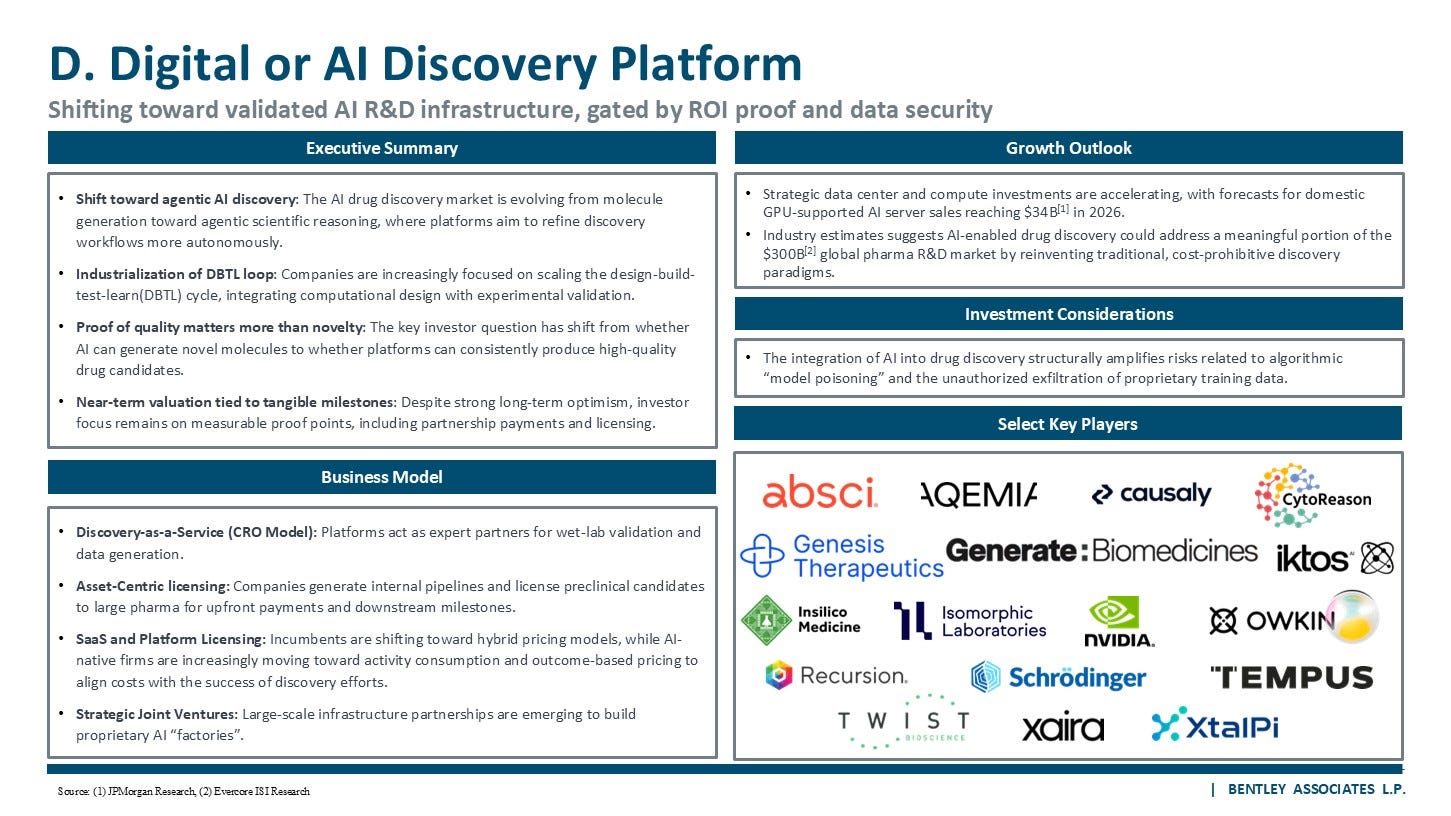

Market Insights: Life Science BioTools (R&D-Focused)

Market Overview

Policy and funding risks weigh on near-term visibility

Macro Environment:

•Pharma R&D remains resilient, but spending is modality-specific — Global pharmaceutical R&D spending is projected to reach ~$250B by 2026, with investment concentrated in next-generation modalities such as GLP-1s, ADCs and cell/gene therapies.

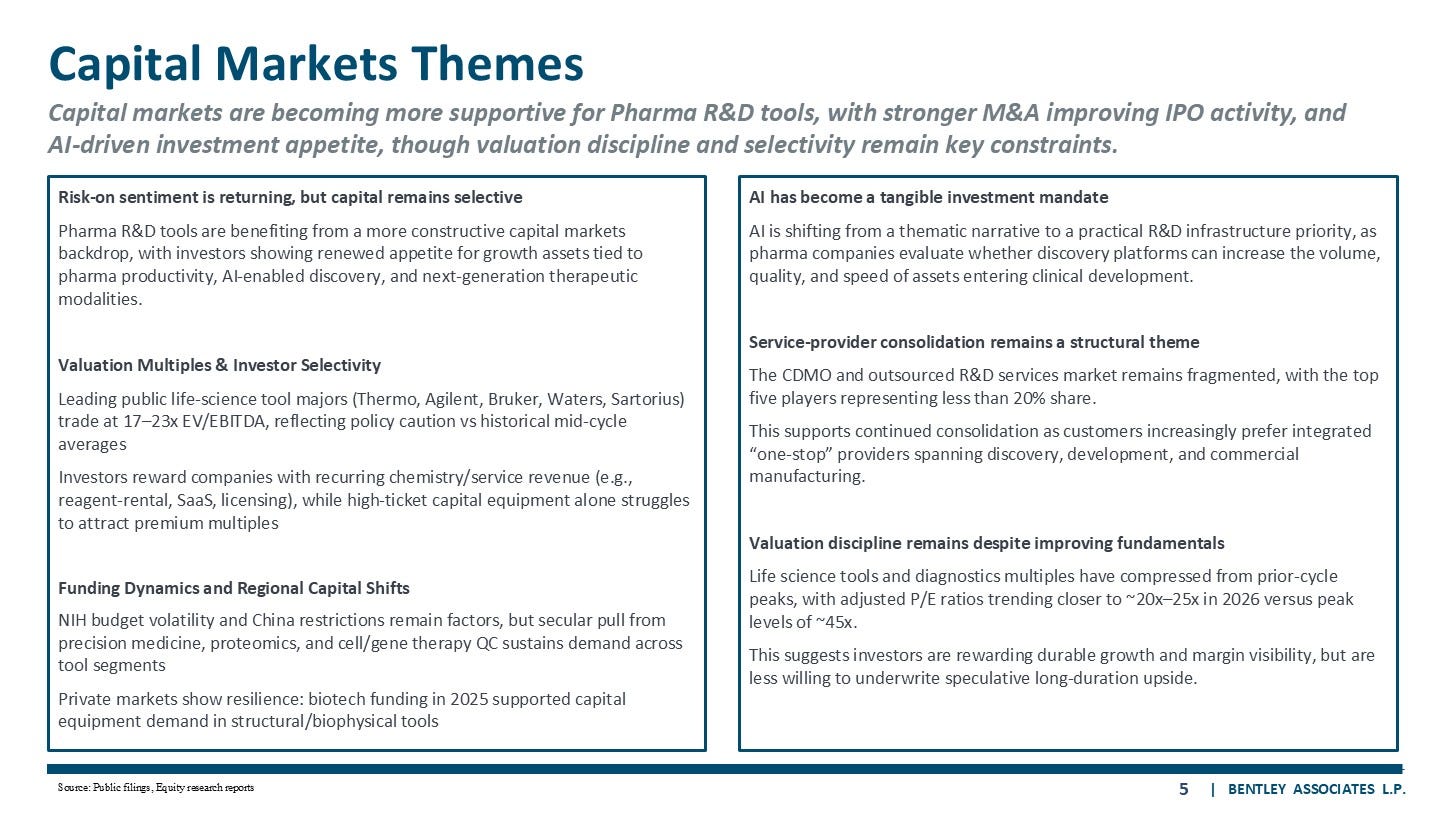

•Biotech funding is rebounding, but selectivity remains high — Biotechnology funding surged in 1H26, up approximately 110%-141% versus the same period in 2025, supporting renewed demand for R&D tools while capital remains focused on higher-quality programs.

•Academic funding risk has eased, but growth remains modest — The finalized FY26 NIH budget included a ~1% increase rather than the previously proposed 40% cut, providing stability for academic and government end-markets.

•Policy overhangs are easing, but pricing scrutiny persists — Greater clarity around IRA drug pricing agreements and pharmaceutical tariff policy has improved customer planning visibility, though drug pricing pressure remains a structural constraint.

•Onshoring creates an equipment tailwind, but timing is back-end loaded — Section 232-related pharma onshoring and U.S.-based manufacturing commitments could provide a 10%-20% boost to hardware and equipment demand, with the impact expected to begin in 2027.

•Margin expansion is being driven by cost discipline— Companies are offsetting muted topline growth through opex control and efficiency measures rather than underlying demand strength.

Market Sizing:

Subsegment Overview